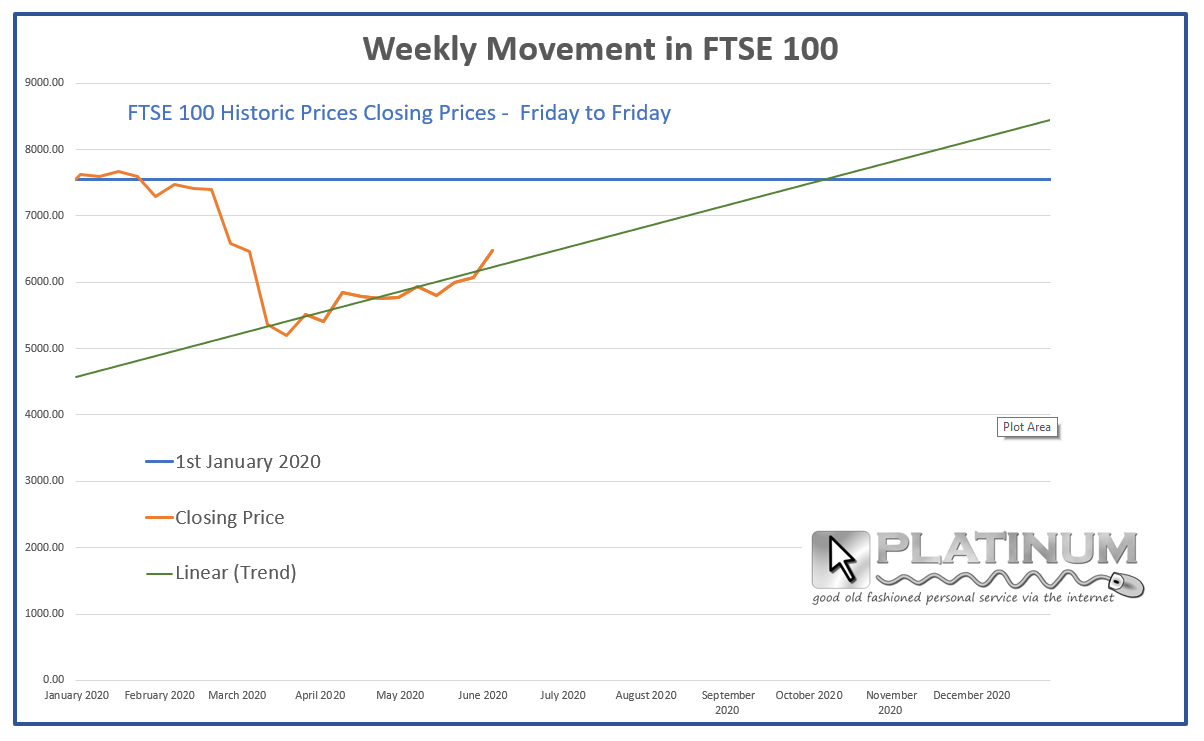

At the start of this year, the FTSE 100 was trading at above 7,500 points. At this stage Corona Virus was something that was happening overseas. Somewhere a long way away!

During January the value of the FTSE 100 actually increased. However during February, the value decreased and stayed just below the opening value at the start of the year. At this stage all deaths had been in China. The first death outside of China took place in the Philippines on 2nd February. By the end of February there were only 20 reported cases of Covid in the UK and nobody had died. At this stage the UK still seemed relatively safe, although European countries were reporting a larger number of cases. Nevertheless, by the end of February the FTSE 100 lost approximately 1,000 points to stand at 6,500 - a fall of 13%.

The first UK death was reported on 6th March. Although the number of reported cases rose, it isn’t until 23rd March that the UK announced a lockdown and 4 days later Boris Johnson tested positive for the virus. During this time the FTSE fell to its lowest point of 5,000 points (a 33% loss since the start of the year). Equally the FTSE 100 had a good 3 day rally with growth of 15% between the 24th and 26th March. In fact the 24th March nearly proved my prediction wrong (of not seeing more than 10% being gained in any one day) as growth of 9.05% was recorded. However the Prime Minister contracting the virus on 27th March brought this rally to an end and markets fell back again.

Since the low point in March the FTSE 100 grew in April and May and thus far in June it has also grown.

What does this mean for me and my pension fund?

Firstly, we hope this shows that the FTSE 100 may be a good benchmark on which to base your plan. So far there seems to be a good deal of synergy between the FTSE 100 index and how the corona virus has impacted on the UK. The darkest days of March are also reflected in the FTSE 100 performance. The early days of panic have gone to be replaced by stoic acceptance. Slowly as optimism has grown in the UK and the lockdown has been relaxed, then the value of the index has started to increase.

Of the 2,500 points lost between the start of the year and the last weeks of March, almost 1,500 have now been recovered. At the close of business yesterday (9th June) the FTSE 100 stood at 6335.72 – this is 15% higher than at the start of the lockdown. The markets are still 16% down on the figures at the start of the year. A further 1,200 points would need to be recovered to get us back to where the markets stood on 1st January 2020.

Is the recovery happening ?

The honest answer here has to be that we don’t know! - but as you will see, the FTSE 100 is heading in the right direction. If the markets do recover this year from their current position to the position at the start of the year, that will mean 16% growth between now and December. The question is – is now the right time for you to switch back into your normal investment options ? Obviously only you can answer that. Many will still be concerned about a second wave of the virus and there is clearly a concern among some that perhaps we are coming out of lockdown too soon and will have to do it all over again. We have no better idea than you.

If you look at the trend of the FTSE 100 (which is not guaranteed) then should the performance from April to today continue then the index would be back to the level it was at the start of the year by October. If you wait until the index is back to its start of year figure, then you would not have benefited from the recovery and you would have guaranteed your loss.

Having said all of this, those who opted for ‘fixed interest’ funds (as opposed to standard ‘cash’ funds) may have done well. We have seen annualised growth of 8% to the year ending 31st March on the Royal London Fixed Interest Pension fund. This is also unusual and unexpected growth and a return that would satisfy most equity investors. However if things return to normal with this fund then you could expect 3.5%.

It is important to remember that the purpose of email is, for those who have transferred into lower risk funds as a result of Covid, to remind them that they will need to review and decide when they should return to a normal investment strategy - ideally in a way that removes the emotion from the decision. If your decision was to reinvest once 2 months of continual growth has been achieved, then you are already beyond this point.

It is important that we state that we are not encouraging or recommending that people reinvest, or move out of cash, but rather we are reminding those who set themselves a FTSE 100 based reinvestment target that their target may now very well have been reached.

This page does not contain personal advice and recommendation based on your circumstances.

The value of your investment can go down as well as up and you may not get back the full amount you invested.

Past performance is not a reliable indicator of future performance.

Investing in shares should be regarded as a long-term investment and should fit in with your overall attitude to risk and financial circumstances.

The value of tax reliefs depends on your individual circumstances.

Tax laws can change.

The Financial Conduct Authority does not regulate tax advice. |